Stablecoin Treasury Management: How Issuers Can Scale Securely

Table of Contents

Stablecoin issuers are stepping into a new era. With clear rules now in place, the next challenge is treasury management that can distribute innovative financial products globally while keeping every token pegged and liquid.

This guide is for issuers, custodians and treasury teams who need to understand how onchain treasury management works in practice. It shows where the risks are, how rebalancing differs from money market funds and what tools make it possible to manage liquidity in real time.

Readers will come away with a framework for faster operations, cleaner compliance and stablecoins that can scale without friction.

A New Day

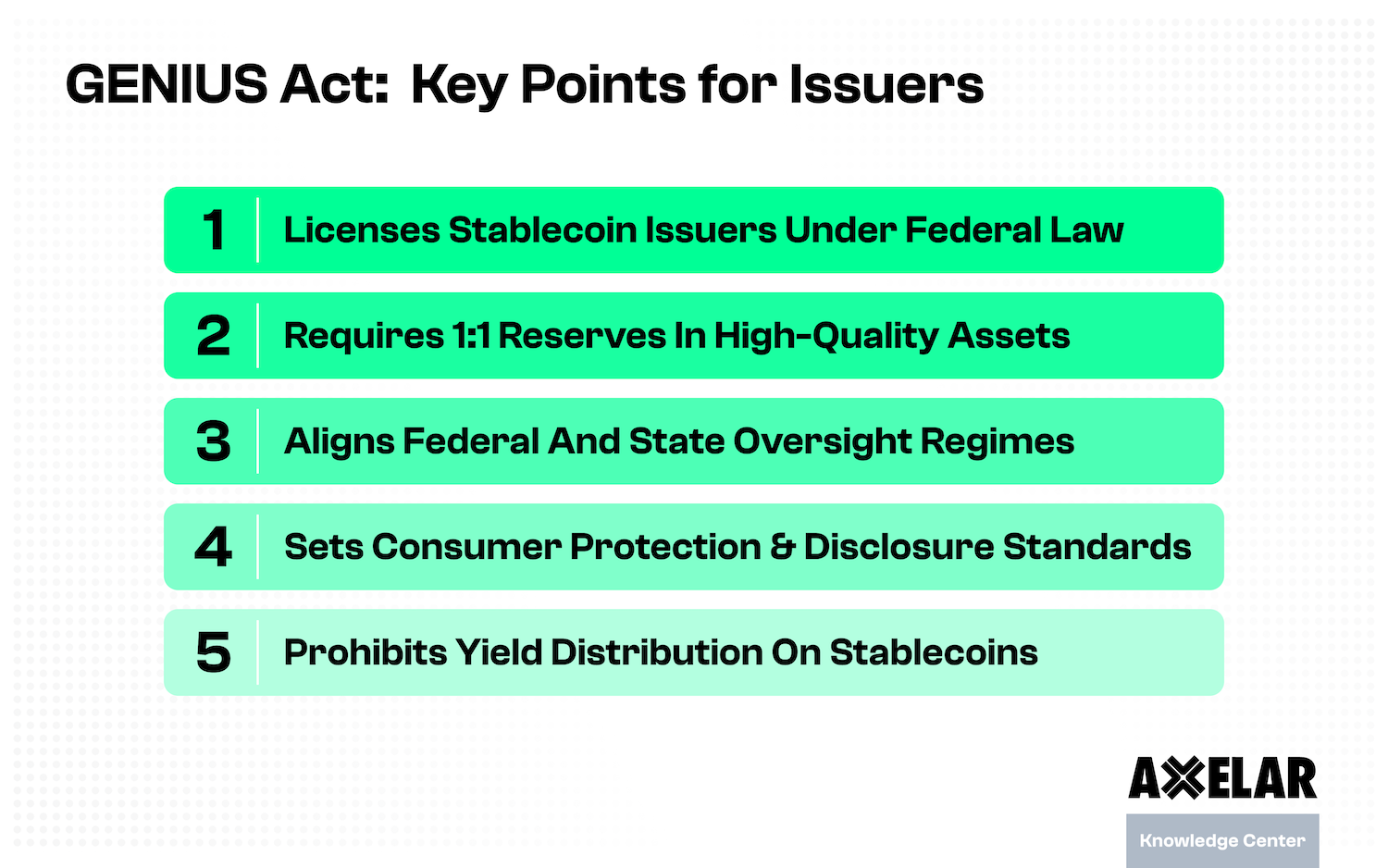

In the last several months, crypto hasn’t just received an invite to the party, it’s become the belle of the ball: everyone, from banks and payment networks to asset managers and corporate treasurers, wants an introduction.1 Of all the party guests, stablecoin issuers are readiest to convert that attention into global, institutional adoption. As Valla Vakili described it, “[stablecoins] represent money’s first real mainstream digital format – capable of being programmable, portable, user-controlled. And if other format shifts are any guide, their impact will be less about reinforcing existing systems and more about unlocking new financial experiences…”2 With the GENIUS Act now signed into law, the US has established a national framework that sets the stage for enterprise-grade stablecoin operations.3 With that foundation in place, stablecoin issuers now need a secure, multichain scaling strategy anchored in interoperability, which enables composability across systems without fragmentation.

Traditional MMF V. Stablecoin Treasury Management

As of mid-2025, stablecoins command over $270 billion in market capitalization, just 1.6 percent of outstanding US Treasury bills, compared with money-market funds (MMFs) that hold more than 40% percent of T-bill supply.4 5 Unlike MMFs, which serve purely as investment vehicles, stablecoins pair the safety of cash-equivalent reserves with 24/7 settlement, programmability and native integration with tokenized markets. These features position issuers to capture significant growth as institutions increasingly adopt stablecoins for payments, treasury, and broader market activity. Yet these issuers must account for how asset and liability management differs from money market funds.

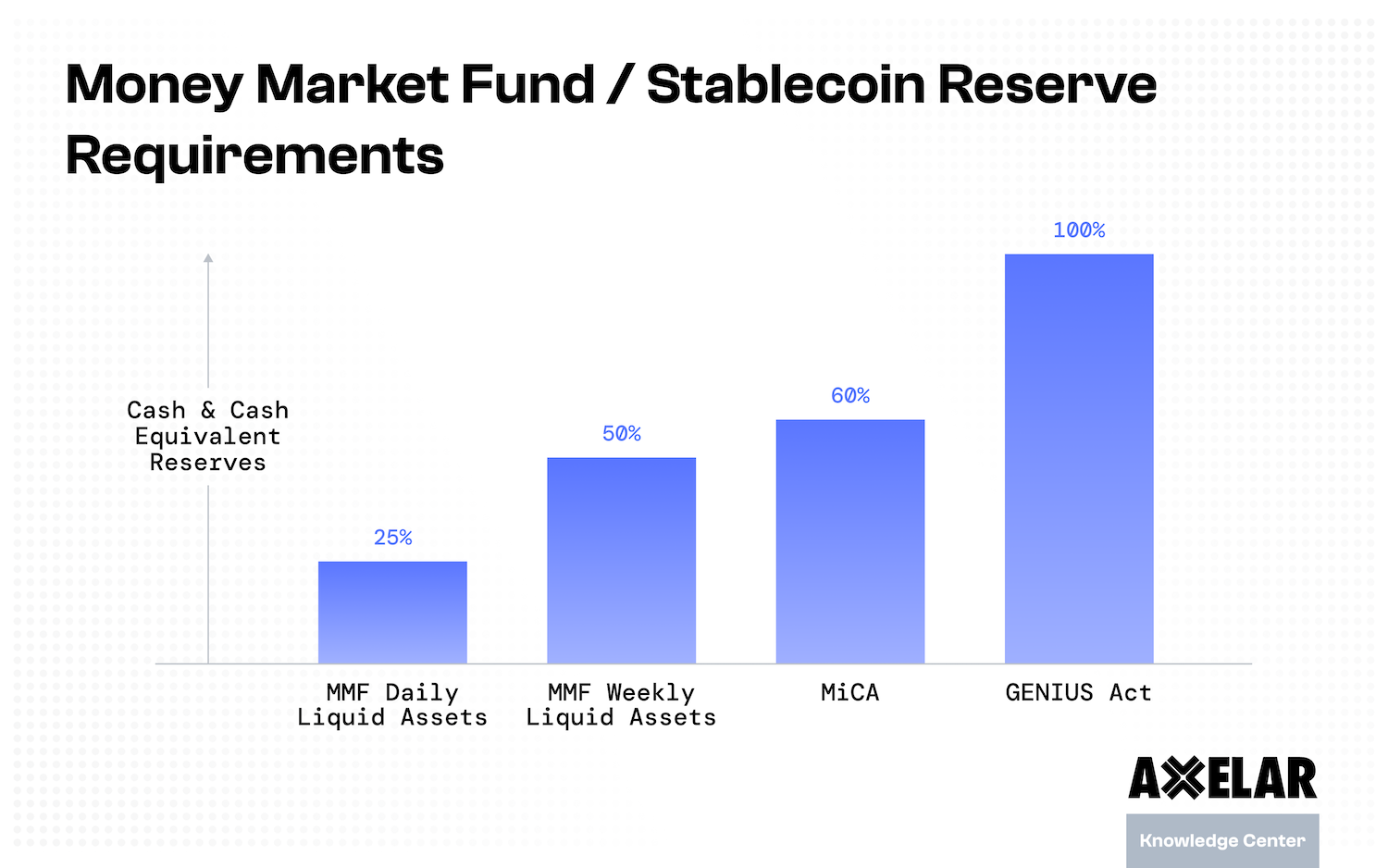

MMFs manage a single, regulated pool of short-dated securities (T-bills, repos, and high-quality commercial paper) with hard maturity limits. Their target is a stable $1.00 share price; if market value slips and the Net Asset Value (NAV) falls below $1.00, the fund “breaks the buck,” an acute event that can trigger large redemptions.

Stablecoin issuers often hold short-dated securities and bank deposits offchain in their reserves. Unlike funds, they keep minted, but unissued, onchain balances in issuer-controlled treasury wallets and decide how much liquidity to seed.6 7 The analogous failure for stablecoins is “losing the peg,” which occurs when tokens trade below $1.00. In these scenarios, restoring the price may require active rebalancing.

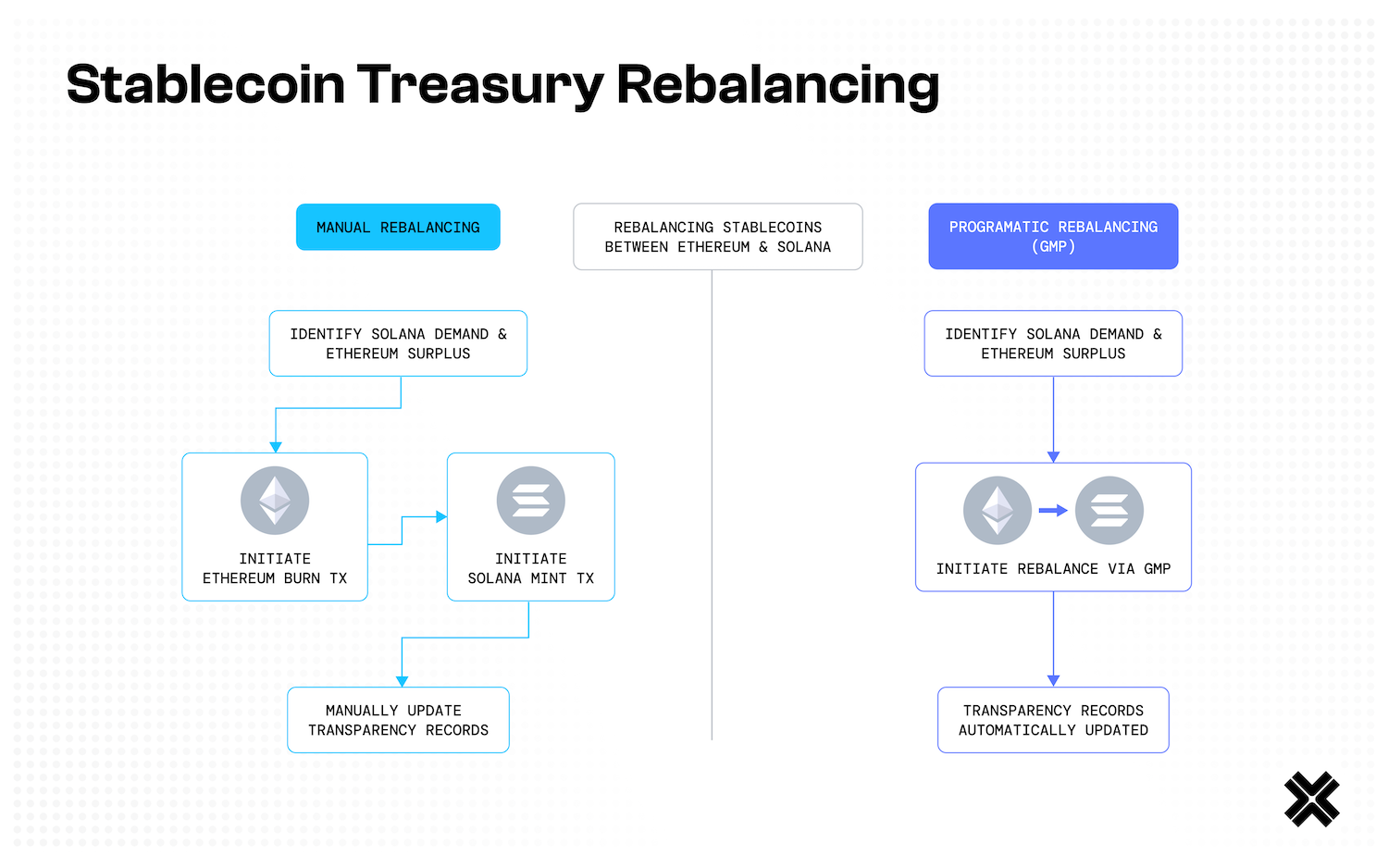

Because blockchains are isolated silos (a token issued on Ethereum cannot be spent on Solana) issuers must keep working balances on each blockchain where their stablecoin is active, and rebalance from treasury wallets. This often requires moving liquidity from one blockchain to another via interoperability protocols (such as Axelar). When one blockchain is short and another has excess stablecoin liquidity, they rebalance by burning supply on the source chain and minting supply on the destination chain, shifting liquidity while keeping total supply constant. By maintaining inventory on each chain and moving it across chains quickly, issuers can minimize delays, prevent price dislocations, and improve liquidity for exchanges.

Attempting to manage liquidity in isolation on each individual blockchain would create fragmentation, increasing operational drag and courting avoidable risk. A multichain connectivity layer can establish a management hub through which issuers can orchestrate burn-and-mint reallocations, enforce policy, and inject liquidity to the target blockchain in real time.

Additionally, in contrast to MMFs, which must keep 25% “daily liquid assets” and 50% “weekly liquid assets,” U.S. stablecoin issuers under the GENIUS Act will be required to hold 1:1 high-quality liquid reserves and provide monthly reserve disclosures.8 The law does not set MMF-style daily and weekly percentage buffers; rather it directs the primary regulators to develop additional liquidity rules. For context, EU’s Markets in Crypto-Assets (MiCA) regulation codifies short-term liquidity proportions of 30% of reserves as bank deposits for “non-significant asset-referenced tokens” and 60% for “significant asset-referenced tokens.”9

Multichain Connectivity Is Critical For Enterprise-Grade Operations

Despite a stablecoin issuer’s reserves sitting in a few bank and custody accounts, its liabilities (i.e., the stablecoins) exist on separate blockchains, requiring rebalancing and chain swaps. Interoperability protocols like Axelar Network address this fragmentation by providing a programmable, decentralized interoperability layer so issuers can coordinate rebalancing from a single place and use compliance logic across chains.

Axelar Interchain Token Service (ITS) and General Message Passing (GMP)

Axelar’s ITS allows issuers to register a token once and distribute it natively across multiple blockchains from a single setup. In practice, ITS deploys token-manager contracts on the blockchains of the stablecoin issuer’s choice to mint, burn, and synchronize supply programmatically. This allows issuers to rapidly expand to any network while preserving transparent accounting of circulating supply.10

GMP allows a contract encoded on one blockchain to call a function hosted on another. Stablecoin issuers can encode rebalancing and trigger mint/burn or transfer on multiple blockchains programmatically, rather than implementing a series of manual functions.11 This enables a singular interface to automate global operations.

How It Works

Example Setup: In this scenario, Ripple (RLUSD) has excess liquidity available in its treasury wallet on Ripple, while demand on Solana is spiking due to an institutional settlement window closing. The following scenarios will demonstrate how the rebalancing process is performed using standard methods versus when integrated with a multi-blockchain token standard (like ITS) and a secure messaging protocol (like GMP).

REBALANCING WITHOUT MULTICHAIN STANDARDS & MESSAGING

- Ripple Treasury Identifies the Imbalance

- Ripple observes that there is an excess of RLUSD liquidity on Ripple and a shortfall on Solana, where settlement demand is rising.

- Manual Burn on Source Chain

- The treasury initiates a burn transaction on Ripple. That transaction is confirmed onchain and confirmed on Ripple’s internal ledgering systems.

- Operational Checks

- The treasury system ensures that reserves remain correctly matched against supply after the reduction.

- Manual Mint on Destination Chain

- The treasury initiates a separate mint on Solana.

- Post-Operations

- Ripple verifies supply consistency across chains, updates compliance and attestation records, and notifies counterparties and liquidity providers of the rebalance.

RIPPLE REBALANCING WITH AXELAR ITS + GMP

- Ripple Treasury Identifies the Imbalance

- Ripple observes that there is an excess of RLUSD liquidity on Ripple and a shortfall on Solana, where settlement demand is rising.

- Single Instruction

- From a single dashboard, Ripple’s treasury issues a seamless rebalance command. GMP packages the instruction, and ITS token-manager contracts automatically execute the burn on Ripple and the mint on Solana in a single flow.

- Audit

- Balances return to target across both networks. The sequence is logged onchain, simplifying Ripple’s reporting and attestation trail.

Looking Ahead

In the post-GENIUS Act landscape, stablecoin issuers have the regulatory clarity to operate at an institutional scale. But doing so will demand more than compliant reserves. It will require an operating framework that eliminates liquidity silos, streamlines rebalancing, and embeds compliance directly into crosschain flows. Axelar’s ITS and GMP provide this infrastructure, enabling treasury teams to manage liabilities across blockchains as seamlessly as moving funds between bank accounts. As Valla Vakili observed, “The companies that build around these new possibilities will determine what finance becomes.”12 Stablecoin issuers now have the tools to be among those companies, and to define the next era of global finance.

1 Deloitte Insights, Crypto is gaining currency with North American CFOs, 31 July 2025, https://www.deloitte.com/us/en/insights/topics/business-strategy-growth/2q-2025-cfo-signals-survey.html

2 Valla Vakili, Redesigning Money: Stablecoins and the Everyday Economy, 11 September 2025, https://www.vallavakili.com/p/redesigning-money-stablecoins-and

3 Library of Congress / Congress.gov, Text – S.1582 – 119th Congress (2025-2026): GENIUS Act, retrieved 15 August 2025, https://www.congress.gov/bill/119th-congress/senate-bill/1582/text

4 IMF, Crypto-Assets Monitor (Q2 2025), 23 May 2025, https://www.imfconnect.org/content/dam/imf/News%20and%20Generic%20Content/GMM/Special%20Features/Crypto%20Assets%20Monitor.pdf (Treasury Secretary Scott Bessent anticipates that Stablecoins could create up to $2 trillion of Treasury debt demand in the next few years.)

5 Goldman Sachs, Top of Mind: Stablecoin Summer, 19 August 2025, https://www.goldmansachs.com/pdfs/insights/goldman-sachs-research/stablecoin-summer/TopOfMind.pdf

6 Tether, Explained: Chain Swaps, 24 October 2019, https://tether.io/news/explained-chain-swaps

7 Board of Governors of the Federal Reserve System, Primary and Secondary Markets for Stablecoins, 23 February 2024, https://www.federalreserve.gov/econres/notes/feds-notes/primary-and-secondary-markets-for-stablecoins-20240223.html

8 U.S. Securities and Exchange Commission, Money Market Fund Reforms (Final Rule, S7-22-21), 12 July 2023, https://www.sec.gov/rules-regulations/2023/07/s7-22-21

9 European Banking Authority, Final Report on Draft RTS to Further Specify the Liquidity Requirements of the Reserve of Assets (Article 36(4)) , 13 June 2024, https://www.eba.europa.eu/sites/default/files/2024-06/580db2f3-8370-4927-baa3-0f995722b417/Final%20report_draft%20RTS%20further%20specifying%20the%20liquidity%20requirements%20Article%2036%204.pdf

10 Axelar Network, Interchain Token Service (ITS), retrieved 1 October 2025, https://www.axelar.network/its

11 Axelar, What Is General Message Passing and How Can It Change Web3?, 29 August 2023, https://www.axelar.network/blog/general-message-passing-and-how-can-it-change-web3

12 Valla Vakili, Finance’s Format Moment: What Stablecoins Make Possible, 22 July 2025, https://www.vallavakili.com/p/finances-format-moment-what-stablecoins