The Stablecoin Liquidity Race: How Issuers Choose Onchain Ecosystems

Table of Contents

This is just a snapshot of the insights in the full State of Stablecoin Liquidity report. Download the full PDF to get all the insights and data.

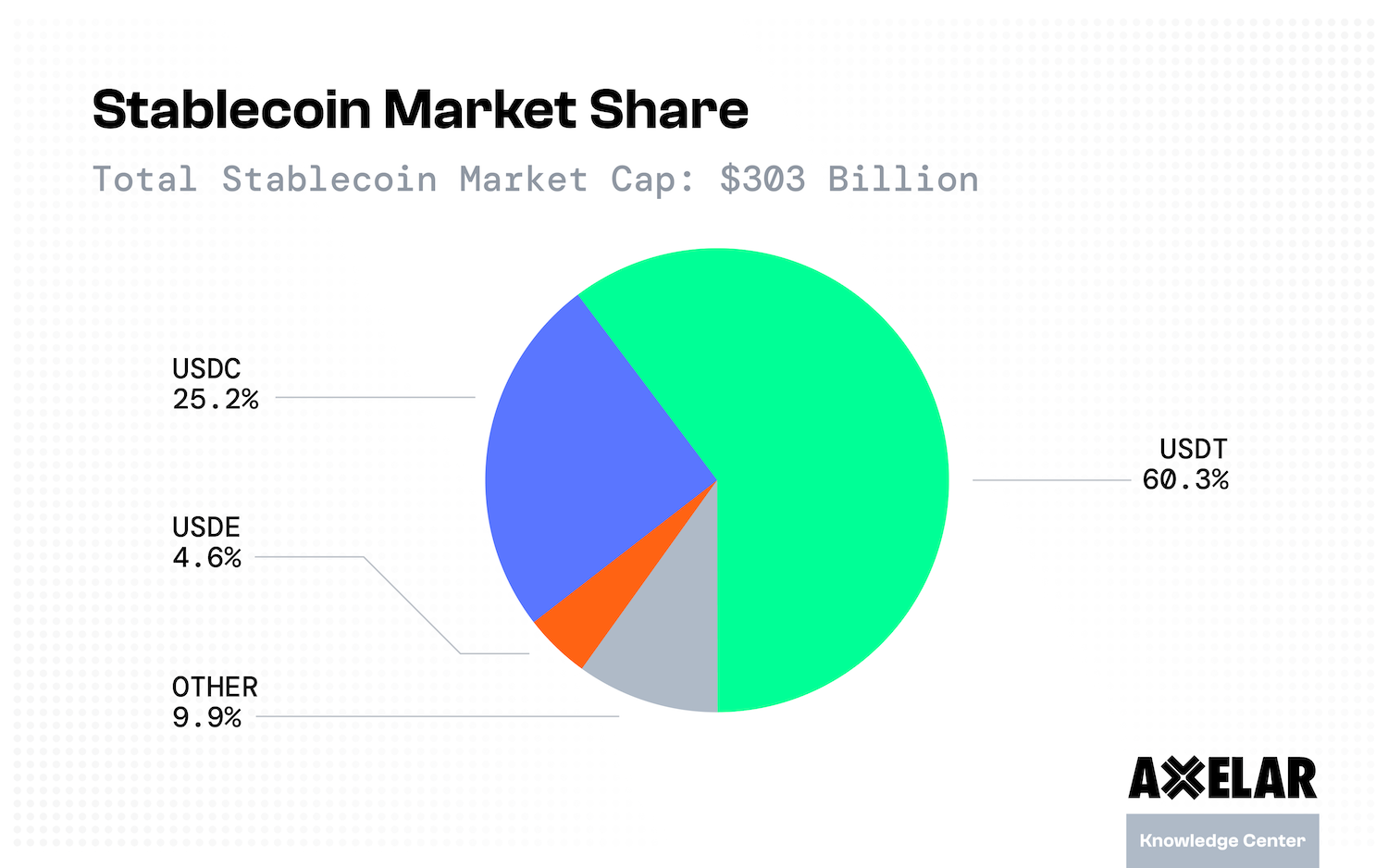

The stablecoin market has reached a pivotal moment. With over $303 billion in circulation and 47% year-to-date growth, stablecoins have become the cash leg of crypto markets, powering trading, lending and payments across the onchain economy.

But this explosive growth has brought a new challenge: issuers now compete for position across multiple issuance platforms, each with distinct user bases, regulatory environments, and use cases. Sustained stablecoin growth will depend on selecting the platforms where utility, regulation, and user demand align to capture market share, extend network effects, and access new revenue opportunities.

Why Chain Selection Matters: Liquidity as a Competitive Advantage

Stablecoin liquidity today is fragmented across both blockchains and competing issuers, creating shallow pools that inhibit capital efficiency.

For investors, this fragmentation translates directly into wider spreads and higher slippage on large transactions.

Issuers understand that deeper liquidity on a given chain leads to tighter execution prices, better user experience, and broader integration with protocols and applications. Network effects compound this advantage: the more liquidity a stablecoin captures on a chain, the more it becomes the default choice for traders and developers.

This dynamic forces issuers to think strategically about deployment, choosing chains where they can maximize liquidity depth, accelerate adoption, and build durable distribution advantages.

The Chain Landscape: Where Liquidity Lives Today

The current stablecoin landscape reveals a stark hierarchy. Ethereum dominates with approximately $150 billion in stablecoin liquidity, cementing its position as the primary ecosystem for onchain finance.

Tron, Solana and BNB Chain have also crossed the $10 billion threshold, emerging as hubs of onchain activity in their own right. But beyond these leaders, the ecosystem fragments rapidly: 11 have surpassed $1 billion in stablecoin liquidity, while 65 chains host more than $10 million in stablecoins.

For issuers, this creates both opportunity and complexity. Each chain represents a different "product-market fit” opportunity defined by its user demographics, primary use cases, compliance requirements, and existing liquidity expectations. Choosing where to deploy means understanding not just total value locked in onchain applications, but the specific behaviors and needs of users on each chain.

When evaluating chains for deployment, issuers weigh three interconnected decision drivers:

Competition: Matching the Chain's Use Case and User Behavior

Different chains attract users with different needs. Ethereum and Solana draw heavy crypto trading and DeFi participation, with users demanding stablecoins with deep integrations with lending protocols and decentralized exchanges.

Blockchains like Tron and BNB Chain offer low-fee, high-throughput environments where retail users prioritize speed and cost for payments over complex financial primitives. For any issuer, the critical question becomes: Can we offer the specific utility users on this chain expect?

Regulation: Where the Stablecoin Can Legally Operate

Jurisdictional considerations shape deployment strategy in fundamental ways. Circle has built USDC around compliance with US regulatory expectations, prioritizing institution-friendly venues and regulated distribution partners.

Tether, by contrast, has captured massive adoption in emerging markets where regulatory frameworks continue to evolve. The proposed GENIUS Act and other regulatory developments will further constrain where certain issuers can grow, particularly for entities seeking to serve US institutions. Issuers must ask: Does the regulatory environment support our minting model and target users?

Risk: Reserve Model, Counterparty Exposure, and User Trust

Reserve structures and redemption mechanisms influence user trust across different markets. Retail users in emerging markets often choose USDT for established liquidity and global reach, even as questions about Tether's reserves persist.

Institutional users, meanwhile, have gravitated toward USDC's transparent reserve structure backed by US treasuries and cash held at regulated financial institutions, in line with GENIUS Act guidance.

Decentralized models like Sky's USDS appeal to users who prioritize onchain transparency and want to avoid traditional banking rails entirely. Each model carries different risk profiles, and issuers must evaluate whether their approach matches user expectations on each chain.

The Future of Blockchain Selection: A Mosaic, Not a Winner-Take-All Market

Stablecoin liquidity fragmentation will persist as new chains, use cases, and geographic markets continue to emerge. Rather than consolidating around a single dominant chain, successful issuers will increasingly treat chain selection as a strategic decision, deploying across multiple ecosystems to reach different user segments.

Solutions providers like Axelar reduce the friction of this approach, making chain selection less about lock-in and more about meeting users wherever liquidity can satisfy user needs. The winners in the stablecoin liquidity race will be those who strategically align liquidity depth, regulatory clarity, user trust, and global accessibility to build durable network effects across the fragmented onchain economy.

Want to dive deeper into stablecoin strategy and distribution? Download The State of Stablecoin Liquidity: Distribution, Fragmentation, and Dominance in 2025.